From the Drudgereport.com

VIDEO: Crazed shoppers stampede at TARGET...

Marine stabbed at BEST BUY...

Shopper arrested after packing gun in belt; knives, 'pepper grenade'...

Mall food court placed on lockdown after fight, reports of gunshots...

Shopper arrested after cutting in line, raging...

Police called after 'thousands' rush TOYS R US...

Woman busted after gun threat at toy store...

Shoppers accuse WAL-MART of false advertising...

The above stories can be accessed from Drudge. We are reaching an extremely sad place in society when we:

1) stay up all night just to spend money

2) disrespect one another for the sake of acquiring material possessions

3) threaten one another over shopping AND finally

4) seriously injure one another for material goods.

We haven't learned our lessons from the current recession to understand what is truly important to us. The "joy" of material goods is extremely short lived. As they say on the FOX Football show "Come On Man!"

(c) 2010 - Jim Lindell

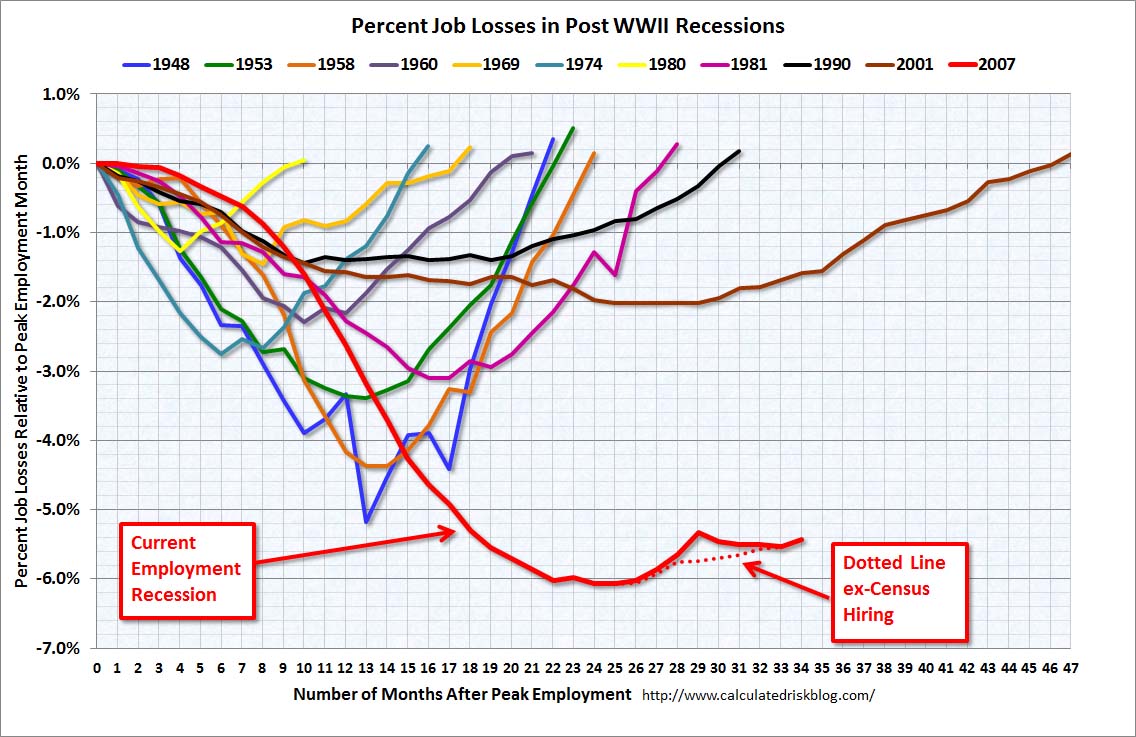

One of the key signs to the economy recovering will be the return of jobs for the unemployed. Since the economy is driven by the consumer, the consumer must have funds (i.e. jobs) to fuel the recovery. The following graph is from http://calcualtedriskblog.com. Note that the previous 11 recessions have followed a similar pattern in terms of job recovery. Unfortunately, the length of time to return to pre-recession job levels in each of the recessions has been getting longer. Also remember that the 2001 recession was known as a jobless recovery. If the trend continues, it does not bode well for the return of jobs. Based on the chart, it does not appear that we will return to pre-recession employment levels for at least a couple of years in the best circumstances. Investors Business Daily used the same information and predicted that the jobs would not return to the same levels until March of 2020. Keep tight reins on your costs. Contrary to the NBER's declaration, we are not out of the recession. © Jim Lindell 2010

Cities Face a Deepening Fiscal Crisis

By Steven Malanga

Source:http://bit.ly/964a36

A recent study of the 77 largest municipal pension systems by finance professors Joshua Rauh of Northwestern University's Kellogg School and Robert Novy-Marx of the University of Rochester estimates that total unfunded liabilities of America's municipal pension systems is well north of half a trillion dollars. On a per capita basis, the professors estimated that each household in the 50 largest cities and counties they studied owes an average of $14,165 for future retiree liabilities. This, of course, is in addition to the other debt these places owe, most especially their municipal debt. New York City taxpayers, for instance, owe about $65 billion of municipal debt on top of what Rauh and Novy-Marx estimate is $122 billion in unfunded pension obligations.....

The city with the highest per household unfunded liability in the nation is Chicago, $41,966 per household, or $45 billion in total obligations....

California is in particularly bad shape. San Francisco and Los Angeles are among the places with the greatest liabilities among cities, amounting to $34,940 and $18,643 per household, respectively....

The implications for taxpayers are staggering as well as retirees. this will force many municipalities to file bankruptcy to try and obtain some relief from the obligations. This does not have a happy ending.

(Source: http://www.newyorkfed.org/survey/empire/empiresurvey_overview.html)

The Empire State Manufacturing Survey indicates that conditions deteriorated in November for New York State manufacturers. For the first time since mid-2009, the general business conditions index fell below zero, declining 27 points to -11.1. The new orders index plummeted 37 points to -24.4, and the shipments index also fell below zero. The indexes for both prices paid and prices received declined, with the latter falling into negative territory. The index for number of employees remained above zero but was well below its October level, and the average workweek index dropped to -13.0. Future indexes generally climbed, suggesting that conditions were expected to improve in the months ahead, although the capital spending and technology spending indexes inched lower.

|

Controller as Business Manager

Controller as Business Manager